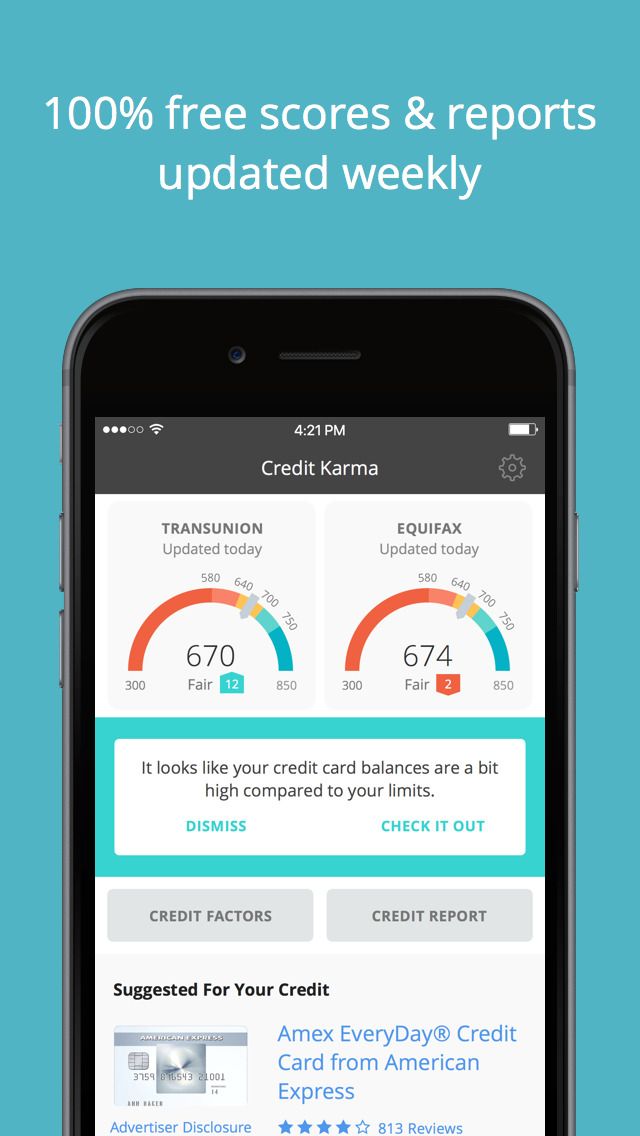

Many financial managers suggest that consumers review their credit reports every year. The process is actually free. It is a great idea to do it each year. Afterward, it's a good idea for any mistakes to be fixed. This should be at the top of your "To Do” list. It is essential to understand the details of your report.

Payment history

One of the most important pieces of data that makes up a credit report is the payment history of accounts you have. This information shows late payments and their severity. Your score will be affected based on the severity and frequency of late payments. The more recent the payments were, the better. A positive payment history is generally a sign that consumers are making their payments on-time.

It is essential to pay your bills on time in order to build a positive payment history. This may mean making some sacrifices but it is essential to build a positive history of payment. Even if you have many accounts, you should still make sure you pay your bills each month on time. It may help to use calendar reminders or autopay to remind you to make your payments. You may have trouble paying your bills if you examine your spending habits and create a budget.

Credit history length

Credit score is affected by how long your credit history has been. Your score will be higher if you have a longer credit history. This is calculated by looking at the average age of all your accounts. Your report will show older accounts more often than the newer ones.

Your credit history is calculated by adding all your accounts together, and then dividing it by the number of years the accounts have been used. The average length of your credit history is about half the time that you can open a new one. Also, opening a new account will result in a hard inquiry to your credit report. You should consider the hard inquiry before you apply for new credit. A hard inquiry can greatly lower your score so it is crucial to act quickly in order to recover.

New credit

It's important to understand the types of inquiries that your credit report might show when it comes to getting new credit. Although you can make several inquiries at once (which is quite common), credit scoring mavens consider them to be one inquiry if they are made within an agreed time frame. This period can range from fifteen to forty days.

Types of credit used

A credit file is a detailed history of your borrowing habits. Consumer credit agencies (CRAs), keep separate files for each customer. Merchants and lenders use this information to determine your risk. These data are used by credit bureaus to determine your risk and give you credit scores.

Age of account

The age of your credit history can play a major role in your credit score. The higher your credit score, the better your credit history. Your account age can be calculated by taking the average of all your accounts and dividing that number by the number. You should also have a mixture of old and new accounts. This will show how you have handled different types of debt. FICO and VantageScore use this information to create credit scores.

A common error people make when interpreting account age is misinterpretation. There are many factors that can influence your account age. It is important to understand the implications of each factor on your credit score.